Bitcoin’s price may appear steady just above $104,000, but activity beneath the surface tells a different story.

On-chain data shows clear signs of a slowdown, with weaker retail participation, falling transaction volumes, and changing investor behaviour. The network itself remains functional and secure, but the dynamics driving market demand are starting to shift.

Analysts from Glassnode, CryptoQuant, and Santiment have released detailed updates showing that everyday engagement has softened while institutional interest remains intact.

This could mark a period of consolidation, or the early stages of a broader change in how Bitcoin is being used and held.

Retail Activity Declines as Institutional Players Step Forward

Glassnode’s recent observations indicate that Bitcoin is entering what they call a cooling phase. The number of active addresses has not increased, network fees have dropped, and overall transfer volume is only moderate.

One of their key indicators, the Spot Cumulative Volume Delta, has turned negative. This suggests that buying pressure in the spot market is declining, particularly from retail traders who tend to drive activity in bull markets.

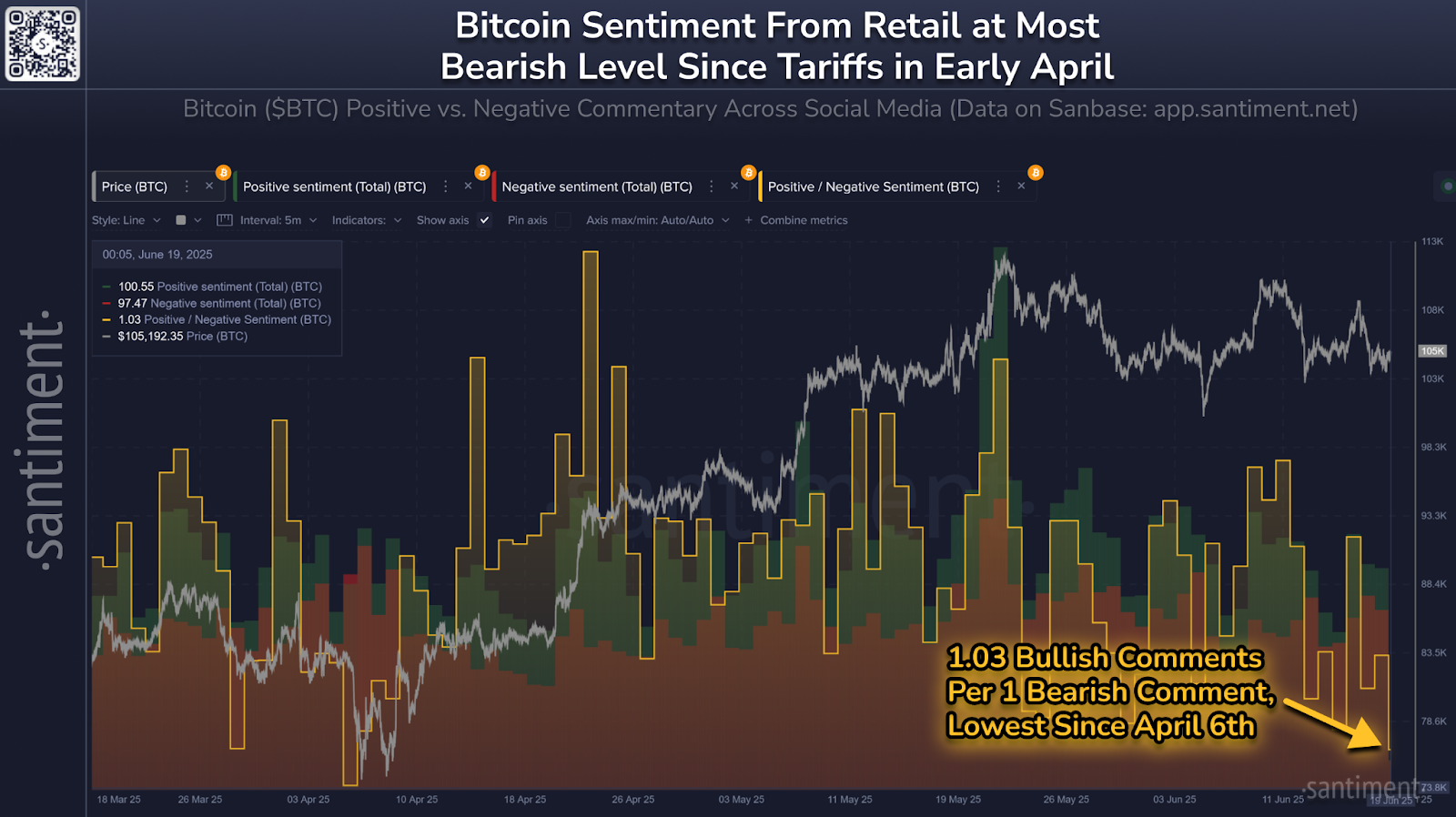

The decline in retail interest is also reflected in broader sentiment. According to Santiment, social media commentary around Bitcoin is nearly evenly split between bullish and bearish views.

The current ratio of 1.03 bullish comments for every bearish one has not been seen since April, when broader market fear reached high levels due to geopolitical concerns.

Meanwhile, smaller holders have been exiting the market. Over 37,000 wallets holding less than 10 BTC have reduced their balances in recent weeks. In contrast, 231 new wallets holding over 10 BTC have appeared, suggesting that larger investors are accumulating quietly.

This shift from many small holders to fewer large ones often signals a consolidation of supply into stronger hands.

CryptoQuant adds that short-term holders, who are usually more reactive to market changes, have sold off roughly 800,000 BTC since late May.

Their demand momentum indicator, which tracks net buying pressure across different investor groups, is now at its lowest point on record: negative 2 million BTC.

This shows a significant drop in overall market conviction, especially from those who tend to enter and exit the market quickly.

However, despite this drop in participation and sentiment, Bitcoin has not seen a sharp price decline. This suggests that while energy in the market may be weakening, there is still enough support to prevent a major reversal for now.

ETF Inflows Continue but Network Usage Remains Quiet

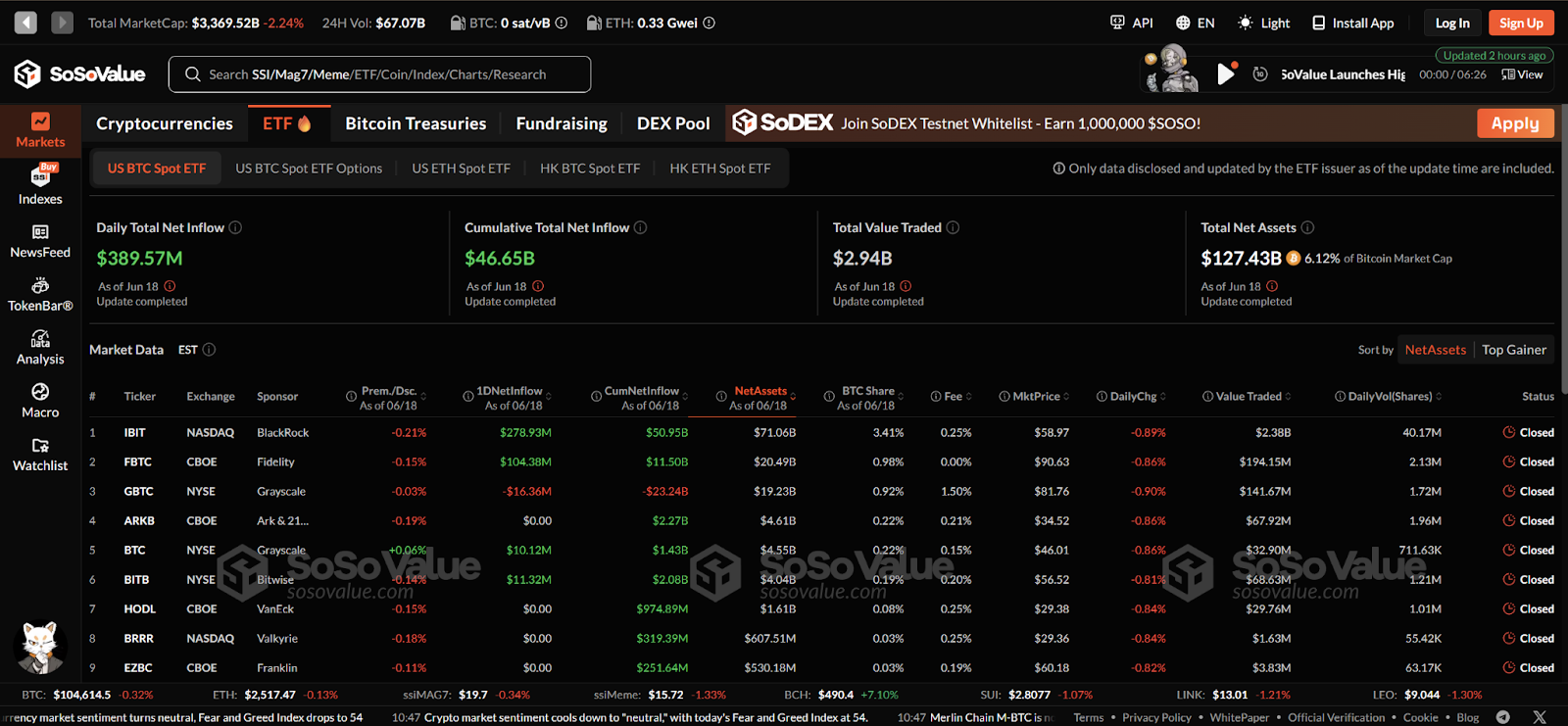

Institutional involvement has remained firm, particularly through spot Bitcoin exchange-traded funds. On 18 June alone, these funds saw nearly $390 million in net inflows.

This marks the eighth straight day of positive movement into ETFs, a sign that institutions are still allocating capital to Bitcoin, albeit in a more passive way.

BlackRock’s iShares Bitcoin Trust led the inflows with nearly $279 million, followed by Fidelity and Bitwise.

These large, regulated investment products are helping institutions gain exposure without holding the asset directly. While they reflect confidence from larger investors, they do not always lead to immediate on-chain activity.

Glassnode highlights this gap. While ETF demand appears healthy, it has not translated into increased use of the network itself. Settlement volumes are still high, but activity is now concentrated in large transactions rather than the many small movements typical of retail trading.

This is consistent with the idea that Bitcoin is now being used more for value storage and fewer daily transactions. Some see this as a sign of maturity.

The derivatives market has also grown significantly, now surpassing spot volume by a wide margin. Futures and options trades can allow for hedging and speculation without requiring coins to move on-chain.

Still, nearly 97% of the current Bitcoin supply is now in profit. This means many holders are sitting on gains, which could be realised if confidence continues to weaken. Without renewed demand from new or returning buyers, the market could face gradual selling pressure.

The structure of institutional involvement is also evolving. Companies like Strategy (formerly MicroStrategy) and Metaplanet are raising funds through unconventional means to accumulate Bitcoin.

These include perpetual preferred shares, convertible bonds, and other instruments that do not rely on margin lending. This approach reduces the risk of forced liquidation but requires careful financial management to avoid dilution or funding problems.

While this method is less likely to collapse under stress, it shifts the risk to areas such as shareholder value and the timing of capital deployment. If managed well, these firms could help support long-term demand. If not, they could introduce new vulnerabilities.

Conclusion

Bitcoin is not crashing. It is not soaring either. It is settling into a quieter state marked by reduced retail activity and a shift towards institutional ownership.

On-chain data shows that while the network is healthy, momentum is fading. Fewer small holders, fewer transactions, and less visible enthusiasm suggest a change in the way the asset is being used.

At the same time, ETF inflows and whale accumulation provide a base of support. Institutions are still active, though in a more controlled and less reactive way. This gives Bitcoin a degree of resilience, even as broader demand softens.